Table of contents

News

News

Posted on

01.04.2026

The generalization of electronic invoicing now places fiscal control in a logic of predictive targeting based on datamining and AI, with an increase in power assumed by the DGFiP in its official press releases. This new environment significantly reinforces the risks of automated detection of VAT anomalies, especially in light of the entry into force of electronic invoicing (e-invoicing and e-reporting) as of September 1, 2026.

1. A tax audit very largely driven by data

As early as 2026, the tax administration will replace ex-post analysis with a proactive targeting strategy based on artificial intelligence. The massive flows of data will feed the algorithmic scoring tools (ALBATROS, FIBRE, SIRIUS PRO) as well as the Mission Requests and Valuation (MRV), a specialized unit of the General Directorate of Public Finances that deploys predictive analysis tools.

The use of these technologies now allows the systemic identification of declarative inconsistencies. The comprehensiveness of e-invoicing and e-reporting data gives these analyses surgical precision, transforming “fiscal data mining” into a real permanent audit of the company.

For companies, this technological change imposes absolute accounting rigor as soon as the invoice is issued, because the targeting of controls, now predictive and documented in advance by DGFiP applications, tends to introduce a de facto reversal of the burden of proof in favor of a tax administration that has become omniscient.

2. Electronic invoicing: a “fuel” for fiscal AI

The deployment of e-invoicing and e-reporting (L. end of 2024) organizes the systematic feedback of transactional data to the DGFiP, via the Public Invoicing Portal (PPF) and the Approved Platforms (PA).

The administration now has a three-dimensional lever for reconciliation:

• Fiscal: Automated comparison between invoice flows (issued/received) and CA3 declarations (VAT collected vs deductible). The same is true with Service Exchange Declarations (DES) and summary statements (former DEBs) for e-reporting transactions.

• Accountant: Verification of the consistency between the Accounting Entries File (FEC) and the archived e-invoices.

• Financial: Cross-referencing of bank data with payment statuses transmitted by e-reporting.

This centralization allows the administration to draw up a “fiscal balance” in real time of the taxpayer, making any anomaly suspicious.

3. Typology of anomalies under surveillance

The administration will make instant reconciliations between data sources that were previously siloed. These machine learning algorithms isolate behaviors that deviate from sectoral standards and will facilitate the identification of certain points of friction such as:

• Sales and purchase cycles: Comparison of invoices issued and received with CA3 declarations to detect discrepancies in collection, over-deductions or unjustified VAT credits.

• VAT anomalies: Discrepancies between the declared VAT collected and the data invoiced, or the application of erroneous rates/unjustified exemptions.

• Documentary integrity: Algorithmic detection of duplicate numbers, sequentiality breaks and chronological anomalies (backdating).

• Cross-banking and third parties: Reconciliation of payment flows with invoices to identify hidden activities, coupled with the exploitation of legal registers and information from platforms (DAC 7).

• International flows: Verification of the consistency of import-export operations by crossing customs data with e-reporting of international transactions.

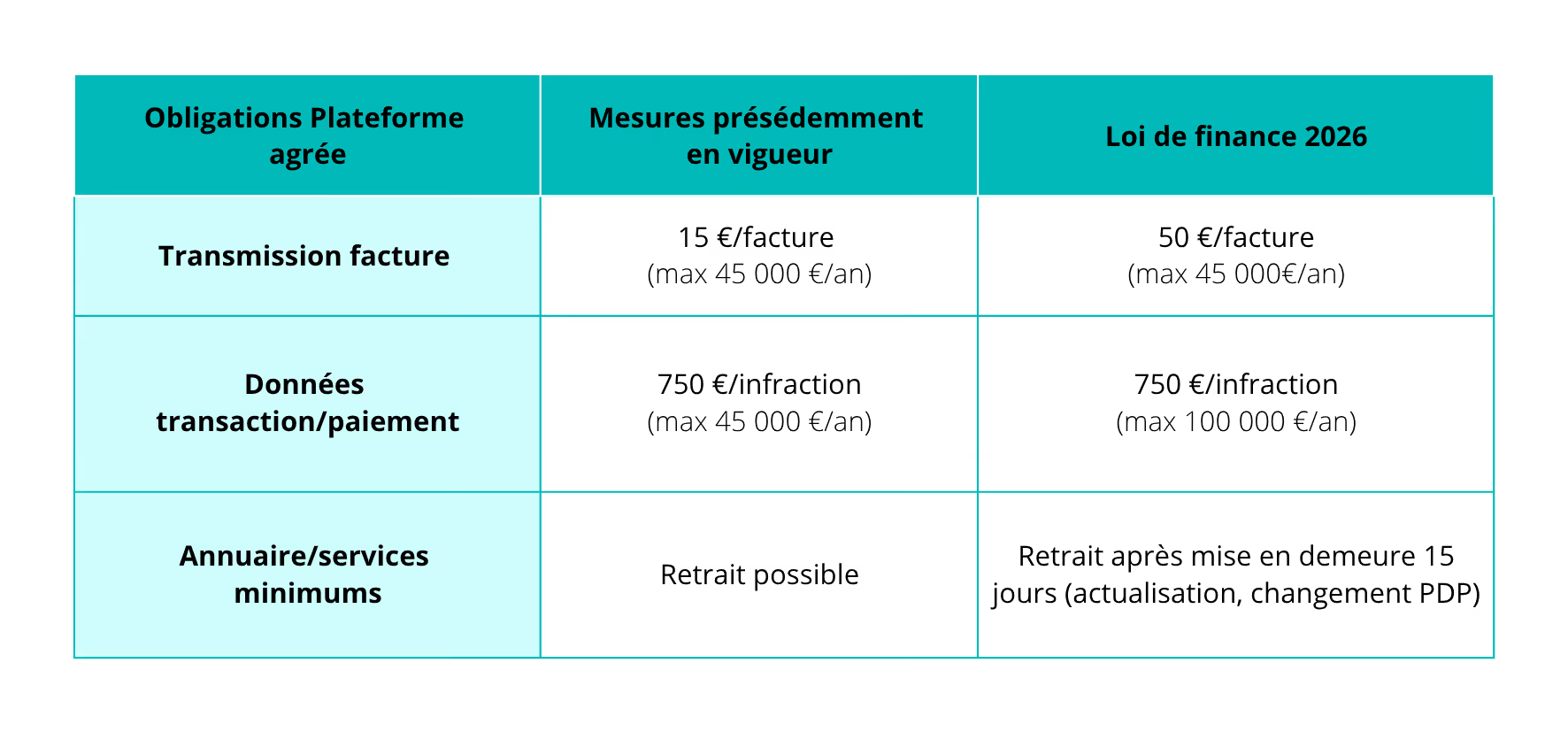

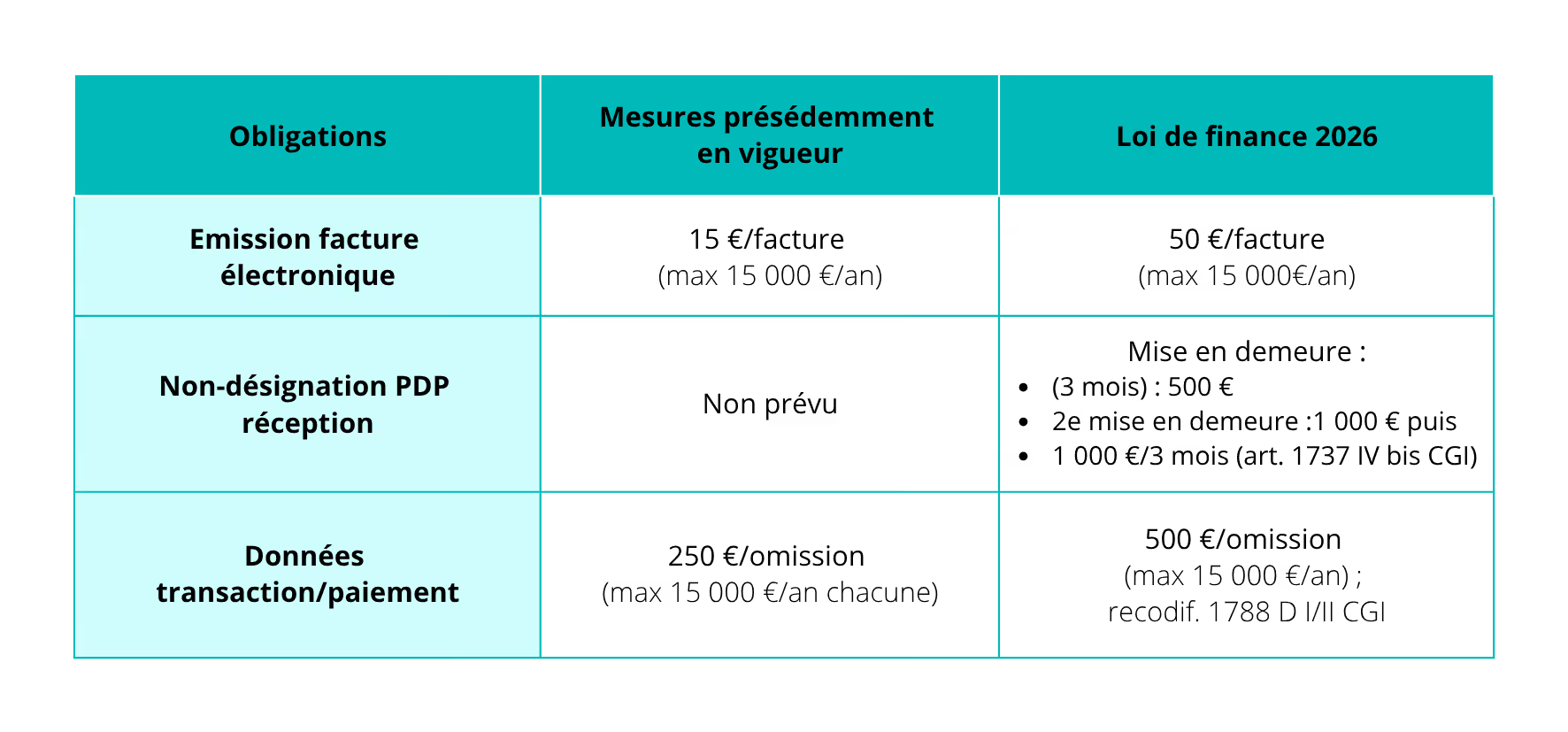

4. Specific sanctions and procedural risks

The finance law for 2024 established a regime of specific administrative sanctions, the thresholds of which were raised in the framework of the 2026 finance law.

The sanctions provided for non-compliance with e-invoicing/e-reporting are increased by the Finance Act for 2026, with increased thresholds and new graduated mechanisms.

Approved Platform Sanctions (PA)

Exemption for first offense is maintained (art. 1788 D V CGI)

Moreover, these regimes of fines and sanctions are combined with existing ones:

• Tax sanctions: These fines are combined with reminders of fees, interest on arrears and surcharges (40% for deliberate breach, 80% for fraudulent maneuvers) resulting from substantive corrections.

• Induced risks: In addition to fines, the administration may question the right to deduct VAT for invoices that do not comply with electronic format.

5. Practical vigilance for businesses

Tax control will no longer focus only on formal regularity, but on the ecosystem coherence of the taxpayer. Tax data becomes real opposable evidence as soon as it is transmitted.

The strategic recommendations to be anticipated now may constitute the following:

• A configuration audit: Verify the conformity of the nomenclature and the VAT rates in the ERPs before any transmission to the PPF/PDP.

• A “mirror” internal control: Set up automatic reconciliation tools (Invoices vs CA3 vs FEC) to anticipate algorithmic alerts from the DGFiP.

• An update of the Reliable Audit Trail (PAF): PAF documentation is becoming crucial to justify complex flows, off-bill discounts or atypical payment terms that AI could interpret as anomalies.

• Increased monitoring of third-party data: Ensure the validity of intra-community VAT numbers and SIRET numbers of commercial partners on a recurring basis.

Actualités

Les dernières actualités